Rubber Stamp Board Of Directors Definition

How To Combat The Rubber Stamp Board Charity Lawyer Blog

Rubber Stamp Definition In The Cambridge English Dictionary

All My New Releases Exciting Or What First Off We Have My Stencils And Red Rubber Stamp Dylusions Rubber Stamp Company Dyan Reaveley

Catslife Press Rubber Stamp Catalog Mail Stamp Snail Mail Snail Mail Pen Pals

Bullet Journal Silicone Stamp Bujo Calendar Date Clear Stamp Weekly Monthly Planner Rubber Stamps Bullet Journal Equipment Bullet Journal Clear Stamps

Made In Arizona Rubber Stamp Hand Lettered Az State Stamp Modern Calligraphy Stamp Southwest Wedding Calligraphy Stamps How To Make Hand Lettering

Rubber stamp definition is to approve endorse or dispose of as a matter of routine or at the command of another.

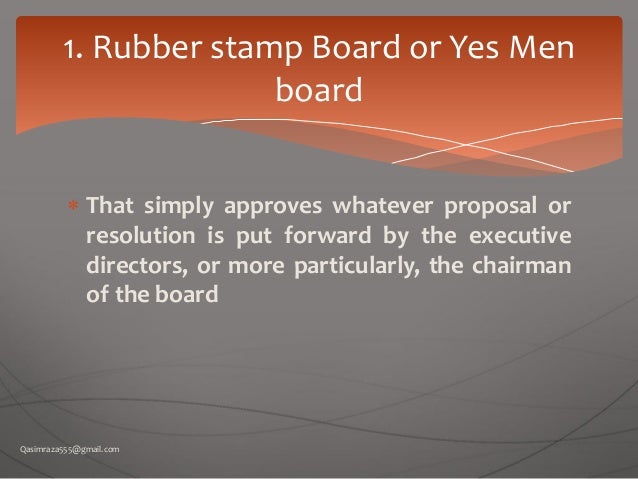

Rubber stamp board of directors definition. Our aim is to provide our customers simple easy. For example shareholders may ratify the decision of the board of directors with little scrutiny. Proprietor director stamps used to put stamp on bill books cheque purpose. A definition of the term rubber stamp board is presented which means a form of board style in which directors act solely to confirm decisions taken by executive management or the holding company in a group.

Thus one way to ensure that a board does not just rubber stamp management s agenda is to educate them about their duties and their potential liability if they fail to fulfill them. Directors are either named in the articles of incorporation or appointed by the incorporator on formation of the corporation. The managing director is the head of the whole management team and a member of the board of a company. Directors who don t take their fiduciary duties seriously risk personal liability for corporate obligations.

The definition of the verb rubber stamp in the merriam webster dictionary is to approve endorse or dispose of as a matter of routine or at the command of another. Directors are often tempted to merely rubber stamp the reports and recommendations of management and committees without exercising their own independent judgment without being rigorous and diligent in. In this case the shareholders act as a rubber stamp to the board. Independent directors who are members of a rubber stamp board are exposed to the risks of being prosecuted for omissions or commissions of the company.

How to use rubber stamp in a sentence. At stampmart you get best quality for proprietor director stamps with free shipping across india most of the orders received by 5 pm are dispatched next working day we have more than 20 years experience we use latest art of technology finest workmanship. It is difficult or rather impossible for directors to directly detect management misfeasance frauds abuse of related party transactions and errors in financial statements.

The Board Of Directors

Bird Defined Rubber Stamp Feather Cards Stamp Bird Cards

Hay Rubber Stamp Company

Charming Pet Paw Print On Heart With Custom Name Rubber Stamp Zazzle Com In 2020 Pet Paw Print Pet Paws Paw Print

Influence Of Intellectual Capital On The Board Of Directors Styles Scialert Responsive Version

Custom Wood Handle Rubber Stamp Custom Stamps Custom Wood Custom

Blog Get Stamped

Managing Director Company Rubber Stamp Ehc Print

Address Stamp Personalized Rubber Stamp Stencil Type By 2impress 19 95 Custom Address Stamp Personalized Stamps Address Stamp

Japanese Name Stamp Custom Rubber Stamp Japanese Stationery Japanese Stationery Custom Rubber Stamps Japanese Stamp

Rubber Stamp English Language Tutorials

Amazon Com Pre Inked Professional Stamp Engineer Architect Business Stamps Office Products

Geometric Rubber Stamp Gemstone Rubber Stamp By Talktothesun 12 00 Artesanias De Tarjetas Sellos De Arcilla Manualidades

Strawberry Rubber Stamp Juicy Strawberry Rubber Stamp Gift For Foodie Jam Making Jam Jar Label Fruit Stamper Berry Fruit Stamp Hand Carved Rubber Personalised Rubber Stamps Rubber Stamp Gift

Rubber Stamp Designing With Eraser And Ink Pad Montage Art Black And White Abstract Ink Art

Stampin Up Greetings 4 You Rubber Stamp Set By Destashavenue With Images Stamp Set Stampin Up Stamp

The Common Seal And Official Seal Of A Co Operative Housing Society

Old Rubber Stamp Font Stamp Download Resume Fonts

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcqdfaurwowijzjko3n40hdnhi 5o Iobabq Wdx7h5mtm8kcdg Usqp Cau

Communication Is Most Important Medium To Interact With Each Other In This World Improve Your Vocabulary By Learning Improve Your Vocabulary New Words Words

Mahjong Tiles 6 1 3 4 X 1 3 4 Mahjong Tiles Mahjong Rubber Stamping Cards

Psx Botanical Viola Violaceae Flower Rubber Stamp By Pollysplace 19 99 Stamp Pyrography Woodburning Projects

Classic Typography Love Conquers All Amour Quote Motivational Words To Live By Modern Stylish Chic This Eleg Love Conquers All Typography Love Typography

Pin On Wish List

Company Chops In China What Are They And How To Use Them

Pin On Livestock 4 H Ffa And Show Signs

Inkadinkado Footprints In The Sand Poem Rubber Stamp 95201 Footprints In The Sand Poem Stamp Footprint

Spring Floral Postage Stamps By Ceci New York Postage Stamp Design Stamp Design Design Stamps

Pin On Music

Cartao De Visita Ecologico By Fischer Portugal Stamped Business Cards Business Card Design Creative Business

Definitely Decorative Bold Butterfly Set Stampin Up Google Zoeken Stampin Up Stamp Set Stampin

3 Twitter Cia Forms Of Communication Central Intelligence Agency

Penny Black Rubber Stamp 1 75 X2 5 Flourish Thank You Joann Penny Black Thank You Images Stamp

Silver Snowflake Stamp 21 05 Stamp Silver Snowflakes Self Inking Stamps

Pin On Christy S Stamping Spot Cards

Social Media Hacks Popular Weekly Weekday Week Day Days Wednesday Friday Hashtags Grow Your In What Is Social Friday Hashtags Marketing Strategy Social Media

Rubber Stamp Making Machine Photo Polymer Easy To Use Youtube

No Title Balloons Stamping Up Cards Cards Handmade

Flaws In The Supreme Court S 101 Precedent And Ways To Correct Them

Hand Carved Stamp Marching Ducks Stamp Carving Hand Carved

Pin By Cristi Doppe On Tattoo 2020 In 2020 Rum Custom Rubber Stamps Stamp